One of the biggest mistakes first-time buyers make is trusting the cash flow number on a listing too quickly.

Because most listings are not showing true cash flow.

They are showing adjusted cash flow.

Usually through something called SDE, or Seller’s Discretionary Earnings.

And buried inside that SDE number are add-backs.

Expenses the seller claims a new owner supposedly will not have.

Some of those adjustments are legitimate.

Some absolutely are not.

To be fair, plenty of businesses have real add-backs.

Those can be reasonable adjustments.

But some brokers stretch these numbers aggressively because higher cash flow supports a higher asking price.

And buyers usually do not realize how dangerous that becomes until the lender starts tearing the financials apart.

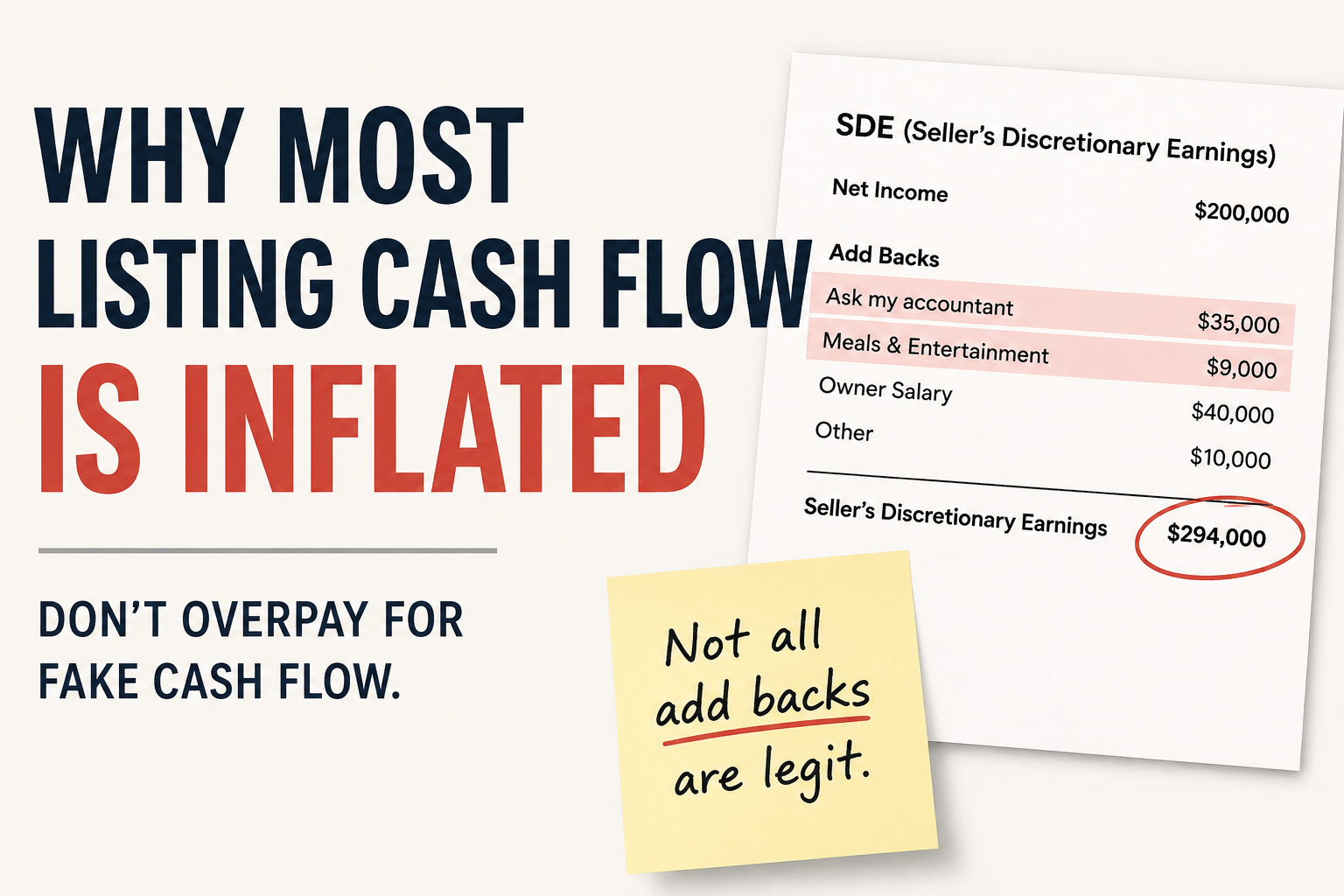

Here is an actual example from a CIM.

One of the add-backs was $35,000 and the explanation literally said:

No breakdown.

No support.

Nothing proving it was actually legitimate.

Now imagine underwriting a business assuming that $35K is real cash flow, only for the lender to reject it completely.

That cash flow disappears immediately.

And because businesses are valued based on earnings multiples, removing questionable add-backs can completely change what the business is actually worth.

There was another line item for $9,000 in meals and entertainment.

The problem is that lenders often only allow around 50% of meals as a valid adjustment.

So that $9,000 may really only be worth about $4,500.

Right there, just two line items created over $30K of potentially inflated earnings.

At a 3x multiple, that is roughly $90,000 of asking price that may not actually be real.

Most buyers fall in love with the headline cash flow before they understand how fragile the number actually is.

But lenders do not care what the broker says the business earns.

They care what they can defend during underwriting.

Once lenders start removing questionable add-backs, the deal changes fast.

This is also why experienced buyers obsess over add-back quality.

Weak add-backs usually signal weak financial discipline overall.

If the seller is stretching earnings aggressively, what else are they stretching?

Before submitting an LOI, go through every single add-back and ask one question:

If you are not sure, assume they will not.

That mindset alone can save buyers from massively overestimating business cash flow.

This is honestly one of the main reasons I built the BizHub CIM Analyzer.

Not to replace due diligence.

But to help buyers pressure-test deals much faster.

Instead of manually digging through PDFs trying to spot questionable adjustments yourself, the analyzer structures the financials, highlights add-backs, estimates SBA viability, and helps surface things that deserve deeper scrutiny.

Because the faster you identify inflated earnings, the less time you waste chasing deals that were never worth the asking price to begin with.