Most people think SBA means 10% down. That’s true on paper. But it’s not the full picture.

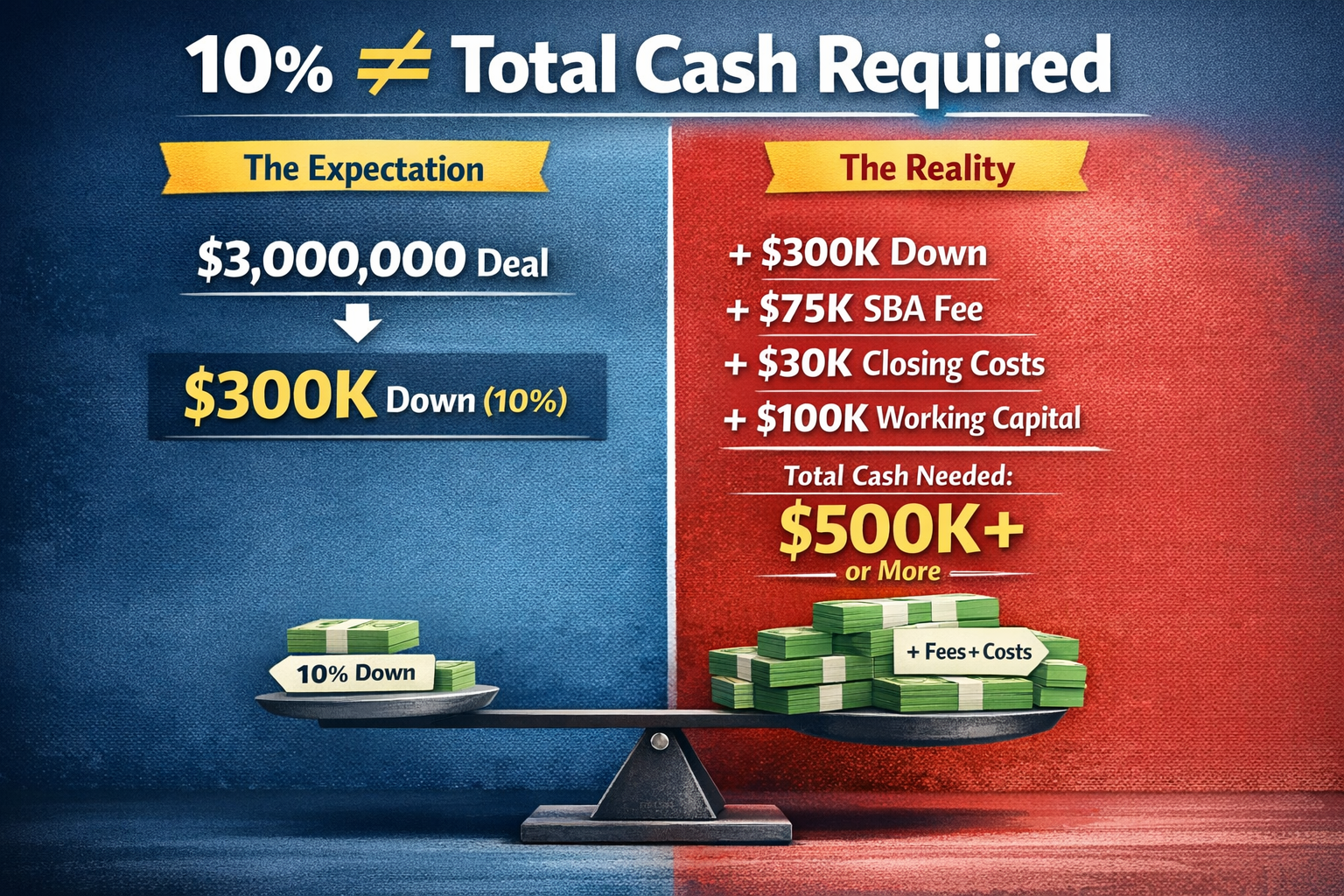

If you are buying a $3M business, the common assumption is simple. You need $300K down and you are good to go.

But the purchase price is only one part of the total project cost.

Base Assumption

That is the number most buyers anchor to. It is also where most buyers get surprised.

What Gets Added to the Deal

In many SBA deals, these costs can be rolled into the loan. That increases the total project size, which means your 10% down is now based on a larger number.

So instead of $300K, your required equity can move closer to $320K+ depending on how the deal is structured.

What Still Gets Missed

Even when these costs are financed, that does not mean you are done with cash requirements.

Most lenders still expect you to have post-close liquidity. That means cash left over after the deal to cover operations, surprises, and early instability.

This is not always a fixed number, but it is often meaningful and can easily add tens of thousands more to what you realistically need available.

What Actually Drives Your Cash Need

- Loan structure: What gets financed vs what must be paid upfront.

- SBA guarantee fee: Usually financed but increases loan size.

- Closing costs: Sometimes partially out of pocket.

- Working capital: May be included, but still impacts lender expectations.

- Post-close liquidity: Cash you must have after the deal closes.

BizHub Takeaway

10% down is a starting point, not the full answer.

Even when costs are rolled into the loan, they still increase the size of the deal and the expectations around your liquidity.

The buyers who get caught off guard are the ones who only plan for the down payment and ignore everything around it.

The BizHub calculator includes SBA fees and helps you pressure test the real structure so you are not guessing when it matters most.

Want to see what a deal actually requires? Run your numbers in the BizHub Deal Calculator →